A Small Compliance Gap That Can Halt Operations

In 2026, GST compliance is no longer limited to filing returns on time. The system now relies heavily on data validation, cross-verification, and automated risk flags. One of the most overlooked triggers for disruption is failure to furnish or validate bank account details on the GST portal.

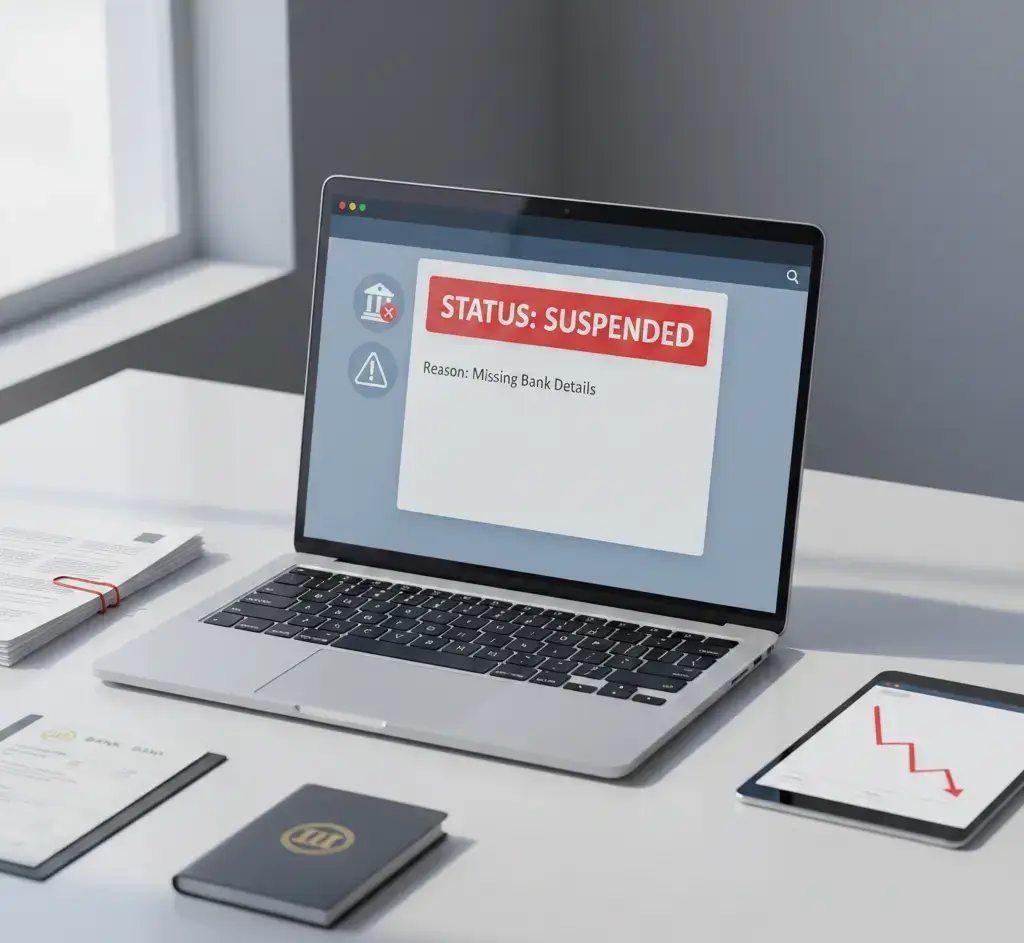

Businesses are increasingly facing automatic GST registration suspension due to missing, incorrect, or unvalidated bank information. The impact is immediate and operationally serious. Suspended GST registration can restrict return filing, invoice issuance, e-way bill generation, and even ITC flow to customers.

This article explains the legal background, the triggers behind automatic suspension, the consequences for businesses, and the exact steps required to restore registration and prevent future disruption.

1. Legal Framework Behind Automatic GST Suspension

Under GST law, authorities are empowered to suspend registration if they believe the registration is liable for cancellation or if compliance risk parameters are triggered.

Rule 21A of the CGST Rules provides for suspension of registration pending cancellation proceedings. Over time, GSTN has integrated automated system-based suspension in addition to officer-initiated action.

There are two primary types of suspension:

System-driven suspension

Triggered automatically based on data risk indicators such as non-filing, mismatch, missing bank details, or suspicious patterns.

Officer-initiated suspension

Initiated manually by a tax officer based on verification or investigation.

In cases involving missing bank details, suspension is typically system-generated. No physical visit or prior discussion may occur before the registration is suspended. The GST portal identifies the risk and temporarily freezes registration until correction is made.

2. Why Bank Details Are Mandatory Under GST

Providing valid bank account details after GST registration is not optional. It is a compliance requirement.

Bank details are used for:

- Refund processing

• Verification of financial identity

• Risk assessment under GST analytics

• Linking GSTIN with financial transactions

After registration approval, taxpayers are required to add bank account details within the prescribed time. Failure to update bank information can trigger compliance alerts.

Additionally, bank accounts must match the PAN linked with GSTIN. Incorrect IFSC codes, closed accounts, name mismatches, or incomplete validation can result in non-verification.

In recent years, GSTN has strengthened bank account validation mechanisms through backend verification systems. This makes incomplete or incorrect information highly detectable.

3. Common Triggers That Lead to Automatic Suspension

Several risk indicators may lead to suspension where bank details are missing or invalid.

Failure to update bank details within required timeline

Incorrect bank account number or IFSC code

Bank account not linked with registered PAN

Closed or inactive bank account

Failure of bank validation process

Repeated return non-filing combined with missing financial details

Aadhaar authentication not completed

In many cases, businesses assume suspension occurs only due to return default. However, missing financial data such as bank details can independently trigger system suspension.

The system identifies incomplete financial profiling as a compliance risk. Once flagged, GST registration status may change to suspended without prior notice.

4. What Happens When GST Registration Is Suspended

Suspension has immediate operational consequences.

Inability to issue valid tax invoices

Restriction on filing GSTR-1 and GSTR-3B

E-way bill generation may be blocked

Customers may not receive valid ITC

Refund applications may be halted

Increased compliance scrutiny

Although suspension is temporary and different from cancellation, business continuity may suffer significantly during the suspension period.

Vendors may refuse to process transactions. Customers may delay payments due to ITC concerns. Ongoing contracts may face compliance clauses triggered by inactive GST status.

5. How to Check If GST Registration Is Suspended

Businesses should proactively monitor GST status rather than discovering suspension during filing.

Steps to verify status:

Step 1: Log in to the GST portal

Step 2: Navigate to Services → Registration → View Registration Status

Step 3: Check status displayed against GSTIN

Step 4: Visit “View Notices and Orders” to identify suspension order reference

If suspension is system-generated, the notice typically mentions reason code. In cases involving bank details, the notice may refer to incomplete or invalid information.

Early detection reduces downtime.

6. Step-by-Step Process to Reactivate Registration Due to Missing Bank Details

Restoration is possible but requires structured action.

Step 1: Update bank details

Go to Services → Registration → Amendment of Registration (Non-Core Fields). Enter correct bank account number, IFSC code, and upload supporting document if required.

Step 2: Validate bank account

Ensure account is active and linked to the registered PAN. Verify correctness before submission.

Step 3: Complete Aadhaar authentication if pending

Incomplete authentication may delay approval.

Step 4: File pending returns

If suspension is combined with non-filing, clear pending returns immediately.

Step 5: Submit clarification if notice issued

Respond through portal within prescribed timeline.

Step 6: Track ARN status

Monitor amendment application until approval.

In many cases, once bank details are validated successfully, suspension is automatically lifted. However, officer approval may be required depending on case complexity.

7. Risks Faced During Suspension Period

Even temporary suspension can create financial and reputational risk.

Cash flow disruption

Delayed receivables

Vendor distrust

Refund blockage

Possible cancellation if unresolved

Audit attention

Businesses must maintain detailed documentation of transactions executed during suspension period for compliance review.

The longer the suspension continues, the higher the risk of escalation toward cancellation proceedings.

8. Preventive Compliance Controls to Avoid Suspension

Proactive compliance reduces business interruption risk.

Immediate bank detail update after registration

Quarterly validation of bank account status

Ensure IFSC accuracy during amendment

Maintain compliance calendar for GST profile review

Monitor GST portal notices weekly

Assign responsibility to compliance officer

It is advisable to conduct periodic GST master data audits covering bank details, contact information, authorized signatory data, and Aadhaar authentication status.

Preventive monitoring is significantly less costly than restoration after suspension. Many growing businesses strengthen this framework by partnering with professional accounting services that monitor GST master data and regulatory updates on an ongoing basis. Companies operating across jurisdictions often rely on structured outsourced accounting services to ensure GST compliance, bookkeeping accuracy, and proactive risk detection before suspension triggers arise.

9. Frequently Asked Questions

Can business operate during suspension

Business operations may continue commercially, but GST-compliant invoicing and return filing may be restricted.

Is suspension the same as cancellation

No. Suspension is temporary pending correction or proceedings. Cancellation is permanent termination of registration.

How long does reactivation take

If bank details are corrected promptly and no other compliance issues exist, restoration may occur within a few working days.

Can suspension be backdated

System suspension usually applies from order date, but underlying compliance issues may relate to earlier periods.

What if bank validation repeatedly fails

Verify PAN linkage with bank, confirm IFSC accuracy, and contact bank branch to ensure account is active and compliant.

10. Strategic Takeaway for Businesses

GST compliance is increasingly data-driven and automated. Technical gaps such as missing bank details can now freeze operations instantly.

Businesses must treat GST master data maintenance as a strategic control function rather than a one-time registration formality.

Bank account validation, timely return filing, Aadhaar authentication, and periodic compliance review are essential pillars of operational continuity under GST in 2026.

Organizations that build preventive compliance systems will minimize disruption, maintain customer trust, and avoid regulatory escalation.